News

Posted date

2016.12.10Analyzing the value of Taiwan's biomedical companies from financial indicators

Audrey Tseng

Deputy Chairman

PricewaterhouseCoopers Taiwan

Analyzing the value of Taiwan's biomedical companies from financial indicators

The value of a biomedical company is linked to its business model

Biomedical was identified as one of the “eight most important technologies” by Taiwan’s government in 1982. Ever since then the government has regarded biomedical as a key industry for Taiwan, as reflected in the 2007 enactment of the “Act for the Development of Biomedical and New Pharmaceuticals Industry” and the 2016 launch of the “Promotion of Innovation in the Biomedical Industry” project. Thanks to this support, the biomedical industry has increased in both scale and maturity. Moreover, many biomedical companies have joined the local capital market; 102 biomedical companies were listed on Taiwan’s stock market as of the end of September 2016 with a total market capitalization of NT$832 billion. However, the biomedical industry is perceived by many to be a high “dream-per-share” sector, which means that stock prices do not match operating revenues or profits of sector companies. Is it that traditional financial statements cannot reveal the value of biomedical companies, or that the details of such are ‘hidden’ elsewhere?

Understand a company’s background before digging into spreadsheets

Every biomedical company has its own way of doing business, and different business models may result in very different types of financial performance. In general, the biomedical industry is categorized as consisting of pharmaceuticals, medical devices and healthcare services. Taiwan’s pharmaceutical companies tend to choose a competitive niche and invest thoroughly in a specific stage of the value chain, unlike international big pharma companies with comprehensive value chains encompassing new drug development, clinical trial, manufacturing and distribution channels. Local companies like PharmaEngine Inc., TaiMed Biologics Inc., Panion & BF Biotech Inc. and TaiGen Biopharmaceuticals Holdings Ltd. license big pharma to leverage their R&D results and earn royalties. The medical device industry covers a wide range of products from advanced surgical devices to eye contacts. Medical device companies use various business models such as licensing and manufacturing outsourcing. Also, some of them make their own products and sell under their own brands.

Biomedical companies have to use distinct profit models and pricing strategies for each business model. Revenue stability may differ, from a new drug developer earning royalties from milestone achievements to a contract manufacturer manufacturing glucometers. The true value of these companies cannot be merely judged by investigating their operating revenue for a single financial period. We will now discuss the use of several financial indicators to evaluate different biotech companies under different business models, as follows:

Useful information derived from business models

A business model typically determines the key success factors of an enterprise, and that of a biomedical company can generally be determined by observing its revenue structure. Furthermore, the growth rate of operating revenue highlights the growth momentum of a company. Gross margins can be used to evaluate a company’s technological capabilities and its future potential. Finally, net income can be used to investigate the ability of management. There are three common business models in biotech: licensing, contract services and retail.

1. Licensing

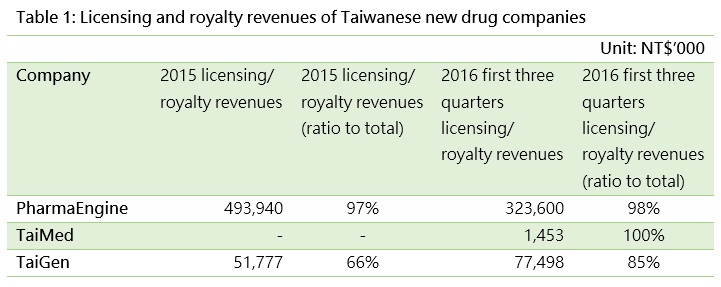

Licensing is popular among new drug developers like PharmaEngine, TaiMed, and TaiGen (Table 1). The earnings achievable from licensing depends on the licensed party and payment method. Licensing big pharma companies to leverage a company’s R&D results is an indicator of a company’s growth potential and future value. If the royalty amount is large, the company may not only receive a higher rate of profit sharing, as the resultant product may also be highly valued and attract more positive views from investors.

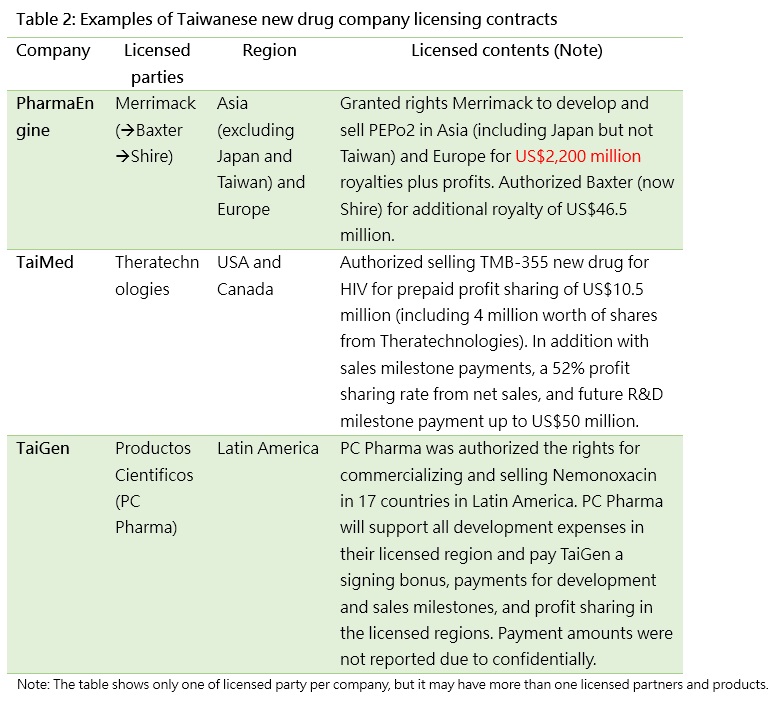

Looking at income from just one period will not show the whole picture, so we need to also examine other information announced by companies as a reference. Such announcements include information such as licensed parties, regions, and contents, and can be used to assess the future growth of an entity (Table 2).

2. Contract services

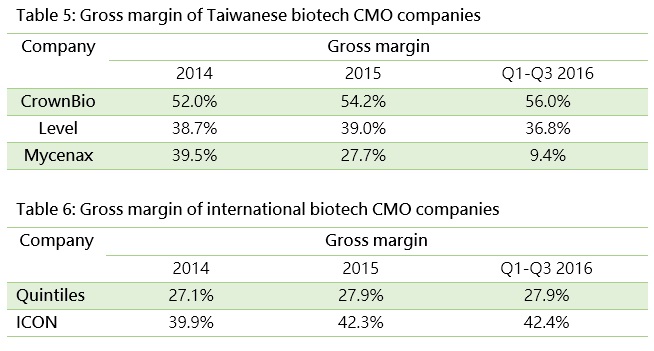

Service revenues are common for biomedical service contractors., such as contract research organizations (CROs) like Crown Bioscience International and Level Biotechnology Inc. which provide research service outsourcing, and contract manufacturing organizations (CMOs) like Mycenax Biotech Inc., EirGenix Inc. and JHL Biotech Inc. which provide manufacturing outsourcing. If a service contractor is not able to differentiate its service, a price war might result and hurt profit growth. On the other hand, if contractors can continuously improve their R&D capabilities and add value to their products, they could enjoy greater competitive advantages and higher gross margins. Therefore, the growth trend of operating revenues, and the value and fluctuation of gross margins are indicators for the growth potential and technological capabilities of biotech companies.

The tables below highlight the key revenue indicators for the CROs and CMOs mentioned above. By operating revenue, CrownBio and Mycenax both enjoy strong double-digit growth. Level Biotechnology has lower revenues, since most of its projects had not been completed during the reporting period.

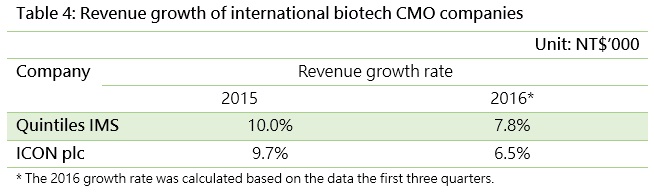

Quintiles IMS Holdings, Inc., the world largest CRO, has a much larger operating revenue than Taiwanese companies, and recorded annual growth of 10% in 2015 and 7.8% in the first three quarters of 2016.

In terms of gross margin, only CrownBio maintained growth to some extent. Its performance for 2016 surpassed even the big pharma companies, primarily because it has the world largest PDX (patient-derived tumor xenograft) and bioinformatics database for diabetes drug analysis, which enables the company to accelerate new drug development ahead of its competitors. Although Mycenax has gained more contracts and increased revenue, its gross margin has declined as its productivity has not yet achieved economies of scale. If Mycenax can scale up, hence its unchanged fixed cost, we would expect a rising gross margin.

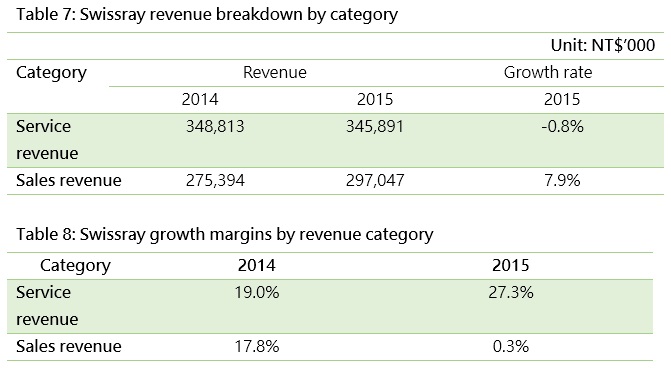

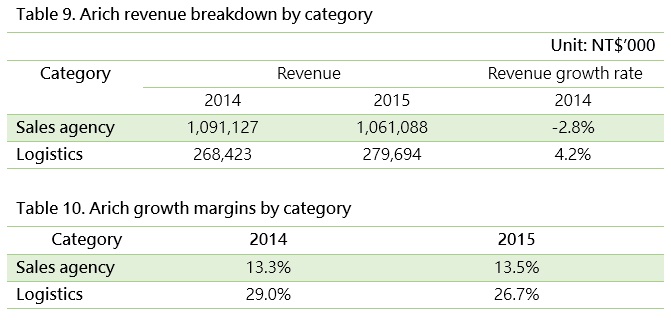

Other service revenue comes from after-sale maintenance and repair services for medical devices (Swissray Global healthcare Holding Ltd.) and administration services for logistics (Arich Enterprise Co., Ltd).

Medical device companies usually sell devices and equipment at low prices to increase their market share, while making profits from selling spare parts and maintenance and repair services. The latter represents 55% of Swissray’s operating revenue for example. As the company is transitioning towards advanced radioactive image diagnostic systems, its gross margin for selling equipment has changed dramatically, while that for its maintenance and repair services has remained stable at around 20%.

Arich is primarily a drug and medical device sales agent but is expanding its business to include medical logistics. Although the sales agency business accounts for 80% of the company’s total revenues, its logistic business is steadily growing each year and enjoys higher gross margin higher than its sales agency business.

In summary, gross margins can reveal the value of a company’s service business.

3. Multi-Channel Product Sales

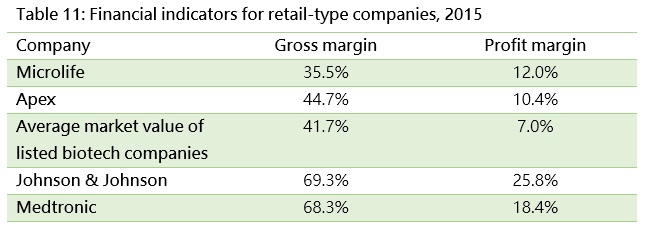

Taiwan’s market is too small for local retailers to scale up. Therefore, many companies look to expand overseas to grow their business and create a platform for a big leap forward. For example, Microlife Corp. and APEX Science & Engineering Corp. have established an overseas presence through merging with international medical device companies. Besides operating revenue growth trends, gross margins can be used to observe a company’s technological capabilities, and net income to assess the ability of management.

Looking at the financial indicators for two international medical device giants, Johnson & Johnson and Medtronic, both have gross margins of about 70% since they have advanced technology and products that match unmet market needs. However, their profit margins are eaten by huge expenses for market expansion. The aforementioned Taiwanese companies which expanded internationally via mergers have higher profit margins compared to general listed companies, though they are still smaller than their foreign peers.

With product bundling becoming more popular, along with the necessity for a high level of marketing expenses, Taiwanese companies have found it difficult to build sales channels in overseas markets. More marketing resources are required. Therefore, investors need to show patience with retail-type companies.

In a nutshell, the value of a biomedical company can be observed from its income statements. When evaluating such a company, one has to understand its business model, identify its key financial indicators, and assess whether it has both the technological capability and growth momentum for a future big leap. By analyzing the information highlighted above, one can develop a foundation for evaluating biomedical companies.

Analyzing the value of Taiwan's biomedical companies from financial indicators

The intangible value of a biomedical company

In the previous article we highlighted how to evaluate a biomedical company by investigating its business model. Now we will look at how to determine the value of a biomedical company’s intangible assets by examining its financial statements.

1. Discover growth momentum through R&D expenses

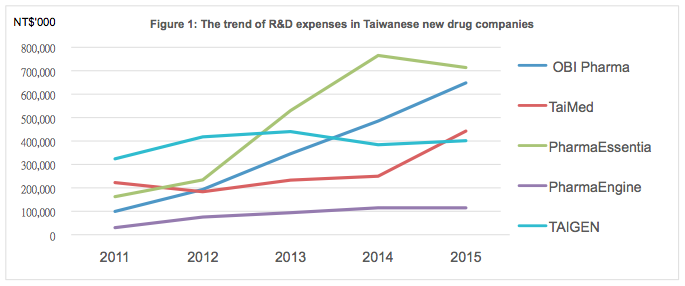

- 1.1 The trend of R&D expenses

Almost all of the top five Taiwanese new drug companies by market value have recorded rising levels of R&D expenses from 2011 to 2015, as shown in Figure 1. Investment in R&D reflects a company’s commitment to the continuous discovery of new knowledge, and innovation in technology, to finding cures for human diseases. Accumulated R&D expense is the fuel that helps new drug companies to grow over the long term, so the market generally takes a positive view of R&D activities.

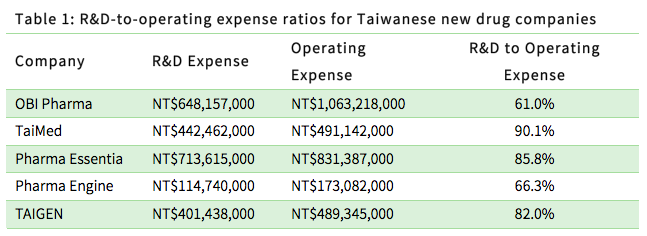

- 1.2 R&D to operating expense ratio- New drug companies

The biomedical industry maintains its growth momentum through R&D activity, so new drug companies can be expected to invest heavily in R&D. The table below shows the ratio of R&D expenses to operating expenses for local new drug companies.

- 1.3 R&D to revenue ratio - New drug companies

- 1.4 R&D to revenue ratio- Generic drug companies

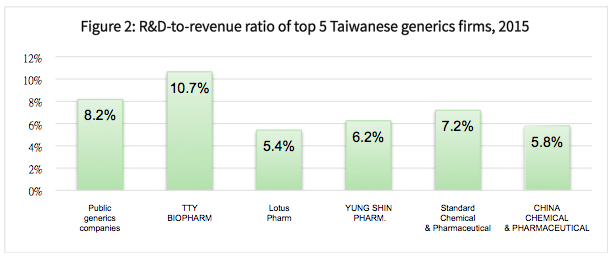

Besides R&D activity, the top five Taiwanese generics companies by market value spend more on selling and administrative activities. Therefore, they generally would not have very high R&D-to-operating expense ratios, but would still need to maintain R&D investment as a certain proportion of revenue to maintain competitive growth.

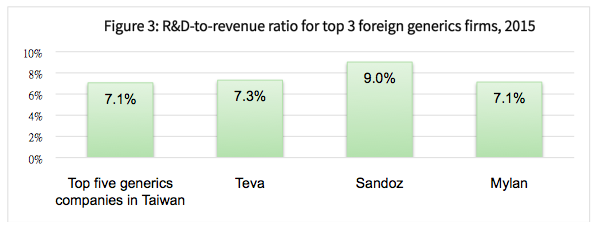

Figure 2 below shows the R&D-to-revenue ratios for the top five Taiwanese generics drug companies, which averaged about 7.1% in 2015. This is lower than the comparative average of 8.2% for all Taiwan-listed generics companies, and also less than the combined average of 7.8% for the top three international generics drug companies (see Figure 3 below).

Given the different business models of new drug developers and generic drug-makers, we can see that their commitment to innovation and growth potential vary accordingly.

2. Intangible assets alone can’t reveal the value of biomedical companies

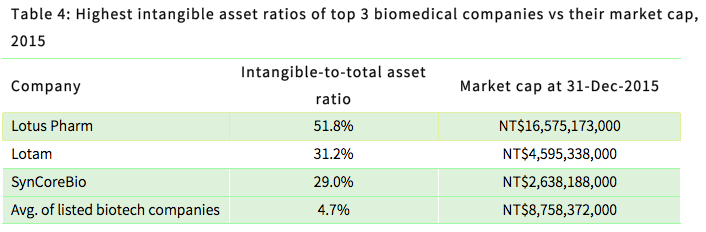

Local investors typically connect intangible assets with the value of a biomedical company. However, under current accounting principles, the full potential of a company’s intangible assets cannot be readily seen in its balance sheet. The only intangible assets that can be observed include acquired licenses, certifications, technological expertise, brand name, and goodwill generated through M&A activities. Therefore, the “intangible assets” that are recorded in a balance sheet do not fully represent the real value of a company’s intangible assets. Indeed, investors should bear in mind that those companies with the highest levels of intangible assets do not match their market cap valuations, as shown in the table below.

Lotam’s intangible assets are mostly acquired drug licenses, and those for SynCoreBio relate to acquired technological expertise for its cancer drug research. Lotus Pharm’s intangible assets are mostly acquired goodwill arising from M&A activities, which is subject to amortization and makes it difficult to assess the real value of the company.

As noted above, the “intangible assets” in a company’s financial statements mostly represent acquired assets, but exclude intangible value generated by internal operations. Therefore, a more comprehensive analysis has to include information from income statements, financial statement notes, corporate announcements and annual reports.

In conclusion, the intangible value of biomedical companies typically come from intellectual property such as patents, technological expertise, drug licenses, goodwill acquired, and internal know-how developed through R&D activities. Each element provides capabilities for a company to grow. When assessing the value of a biomedical company, investors should look at whether it has accumulated any technological capabilities. Other considerations include the risk of the impairment of intangible assets. Integrating each aspect allows for a more comprehensive assessment of a company’s value.